This is an addition to the previous post in which we have analysed oil prices based upon fundamentals estimates based on supply & demand. As anticipated in the same post we have warned against large changes in prices due to other variables such as geopolitics.

Since our last post the price of OIL has continued its down spiral and as of today we are sitting at a 5 ½ years low.

We would therefore like to shed some light on the current variables at play and also advise on the non sustainability of such pricing in the long run. These are exceptional times and they should be treated as such.

Variables currently pushing the OIL price down:

Since our last post the price of OIL has continued its down spiral and as of today we are sitting at a 5 ½ years low.

We would therefore like to shed some light on the current variables at play and also advise on the non sustainability of such pricing in the long run. These are exceptional times and they should be treated as such.

Variables currently pushing the OIL price down:

- Policy of containment towards Iran, Syria, Islamic State and Russia adopted by OPEC Gulf States;

- OPEC members interest in slashing fracking projects profits and delay or contain their production;

- Weaker than expected Chinese economic performance although we believe that the current statistics with regards to economic performance are not justifying the current price drop;

- Weaker demand demand than expected from the US side.

In spite of the large reserves of some OPEC suppliers trapped into their Sovereign Funds, many of these countries have set up their countries expenditures and development against a higher price per barrel. Please be reminded that these countries are tax free regimes and their economic performance and development plans are affected directly by the price of OIL.

Further, a low OIL price and a strong dollar combination is going to hurt significantly all development projects in the Oil & Gas industry that are financed in USD, something clearly undesirable for many powerful US lobbies.

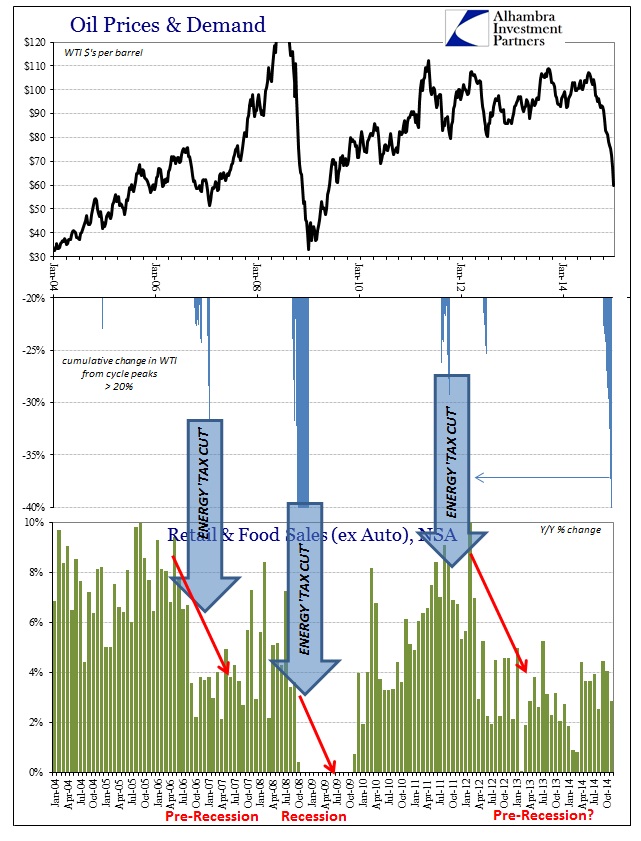

Lastly, while the mainstream media in the USA are hailing the low OIL price as a welcome stimulus to the economy this will not turn into reality. The US is facing a lethargic demand that is not supporting the recovery picture portrayed on the media. Please note that statistically any time that there was an energy tax cut in the US there has been no subsequent sign of positive stimulus afterwards.

Because of the above listed reasons we believe that the current significant price drop is temporary and far exceed the drop potentially justified by a weak US and partial restatement of Chinese growth.

We would only expect OIL at current price for a protracted period of time in the face of a recession 2009 which could be fought once again by the Feds with a new and improved set of QE cycle.

No comments:

Post a Comment